March 19, 2026

What Experienced Buyers Ask Before Buying an Online Business

But there is an important distinction many sellers and buyers overlook:

MRR is not the same as business valuation.

MRR is a useful metric. In many cases, it is one of the first numbers people look at when evaluating a SaaS product or subscription business. Still, it only tells part of the story. A business with strong MRR can still have weak margins, high churn, poor retention, or unstable operations. In those cases, the actual value of the business may be far lower than the headline revenue number suggests.

Understanding this difference is essential for anyone preparing to sell, buy, or assess a digital business.

MRR, or Monthly Recurring Revenue, measures the predictable revenue a business earns each month from active subscriptions. For example, if 100 customers each pay €50 per month, the business has €5,000 MRR.

MRR gives a normalized monthly view of recurring income. It is especially valuable for businesses built around subscriptions because it shows whether the revenue base is becoming stronger over time. However, MRR is a tracking metric, not a complete valuation model.

The biggest problem with relying on MRR alone is that it only looks at recurring top-line revenue.

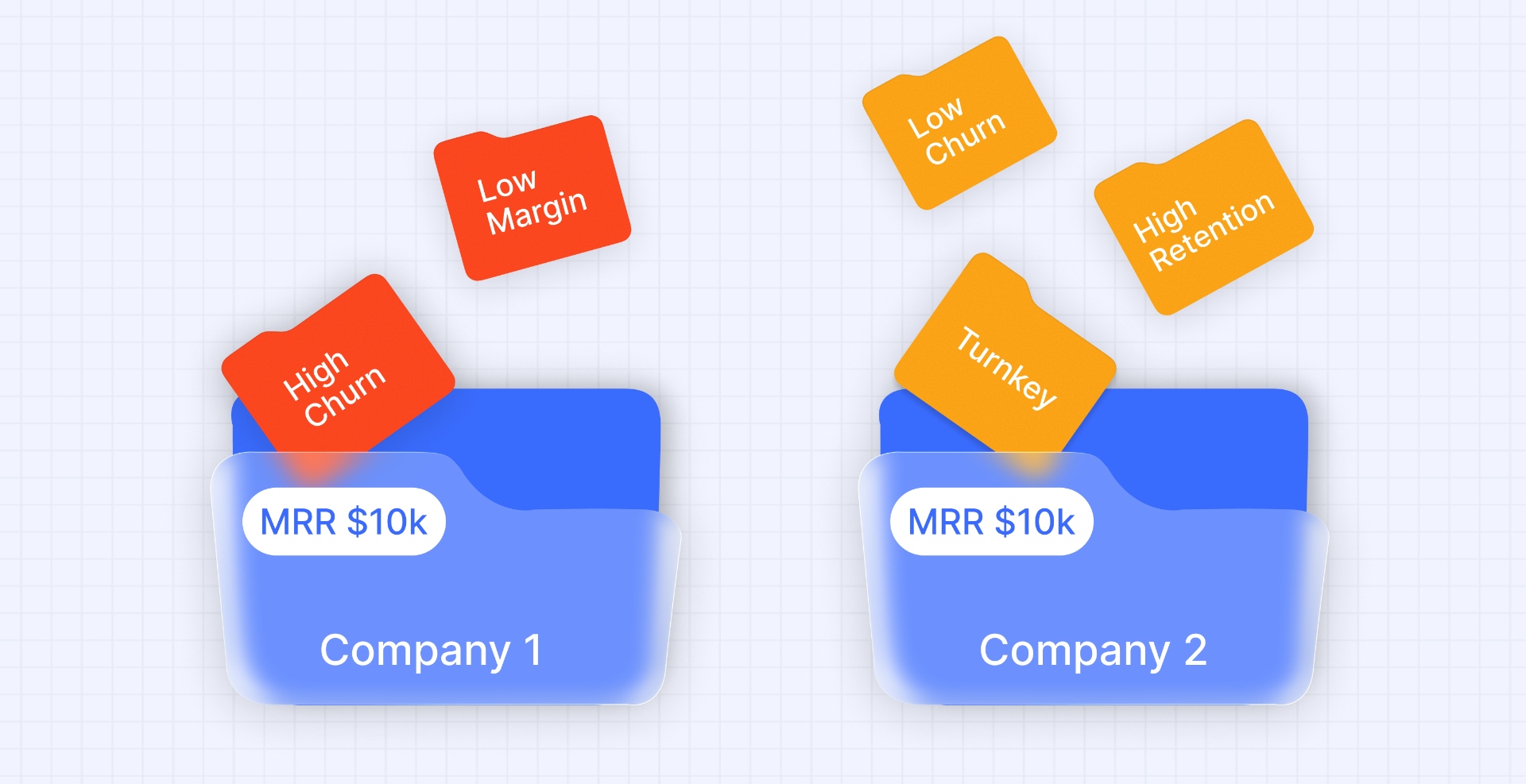

Two businesses can have the exact same MRR and still be worth very different amounts. One may have strong retention, efficient growth, and clean operations. The other may be losing customers quickly, spending too much to acquire users, or relying on short-term demand. On paper, both show similar recurring revenue. In reality, they carry very different levels of risk. That is why MRR should be seen as a starting point, not the final answer.

Not all recurring revenue has the same value. A business with stable subscriptions and low churn is far more attractive than one with the same MRR but frequent cancellations. Buyers and investors care about the quality of revenue, not just the size of it.

If revenue is recurring but unstable, its value drops. For example, €20,000 MRR may sound impressive, but if a large share of users leaves every month, the future revenue base becomes uncertain. In that case, the business will often receive a lower multiple because the recurring revenue is not truly durable.

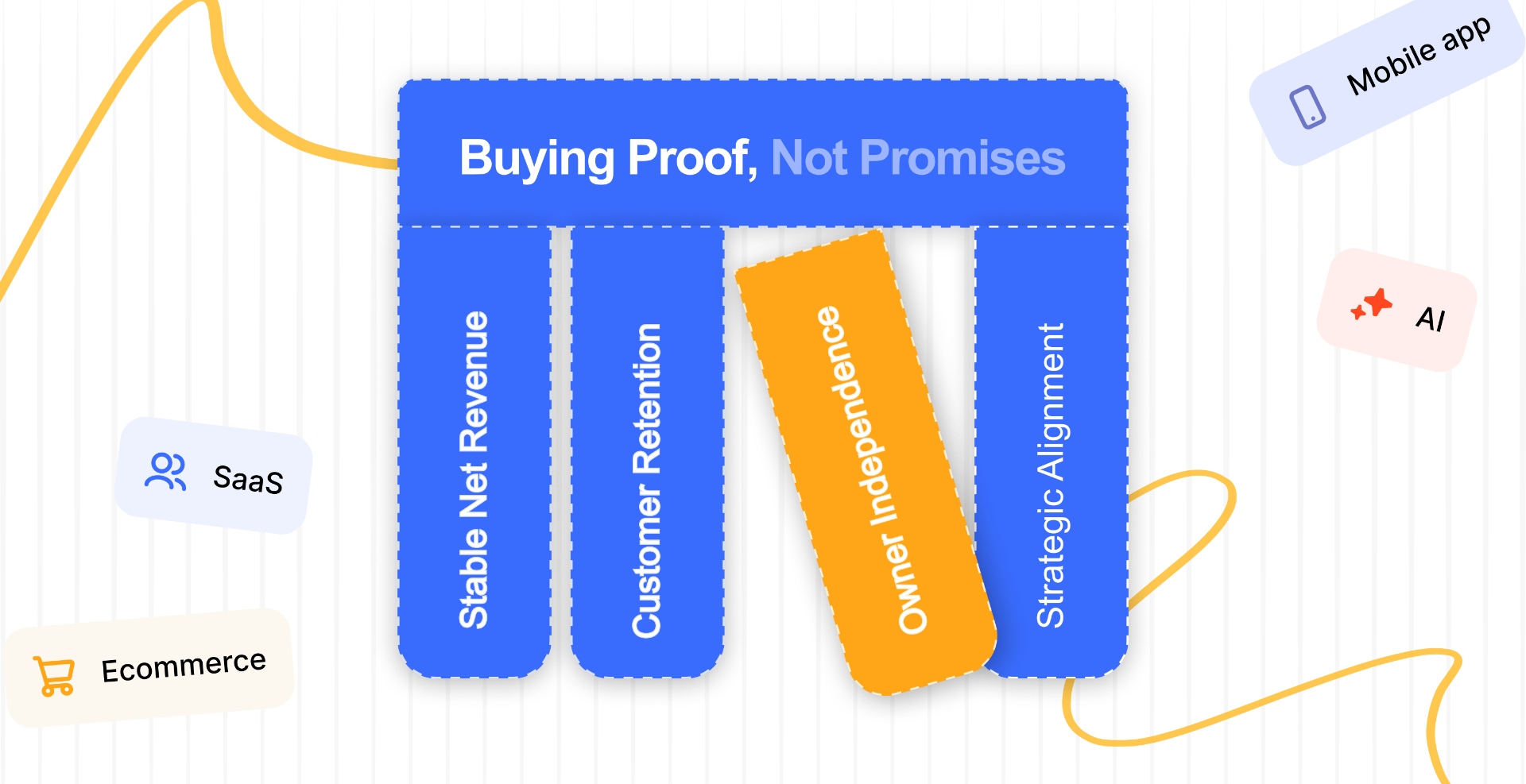

Real business valuation is broader than recurring revenue. A proper valuation considers not only income, but also the structure and durability of the business behind it. That includes financial, operational, and strategic factors.

This is why valuation multiples vary so much from one business to another. A business with healthy margins, low churn, strong processes, and clear growth opportunities may command a premium. Another business with the same MRR but weaker fundamentals may be valued far lower.

One of the most common mistakes founders make is assuming that MRR automatically translates into business value through a simple multiple. In reality, valuation is always contextual.

Without that context, MRR can create false confidence. A business may look strong because the top-line metric is growing, while deeper analysis reveals that costs are too high, customer retention is weak, or growth depends on one unstable channel. In those cases, the real valuation may be much lower than expected.

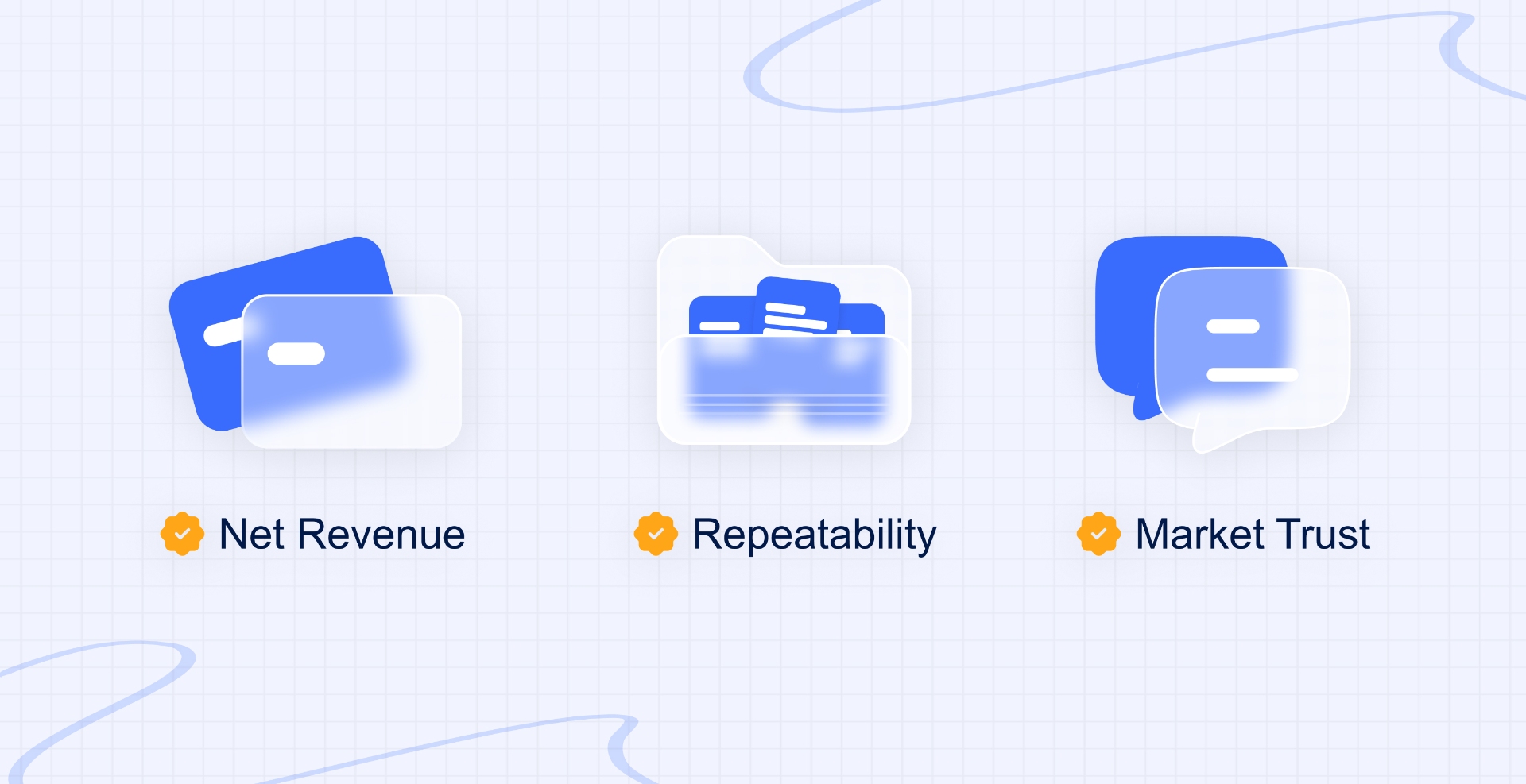

MRR is important, but it works best when paired with other metrics that show business quality.

This gives a clearer answer to the real question:

Is this recurring revenue stable enough to support future value?

That is what buyers ultimately care about.

MRR is one of the most useful metrics in subscription businesses, but it is not the same as real business valuation. It shows recurring revenue strength, but not the full health, resilience, or scalability of the company. Real valuation depends on the quality of that revenue, the efficiency of the business, and the long-term risks and opportunities surrounding it.

In simple terms:

MRR is part of the story. Valuation is the full story.

For founders, that means recurring revenue should never be presented in isolation. And for buyers, it means the smartest decisions come from looking beyond the monthly number and understanding the business that produces it.

.svg)